England and America are two countries divided by a common language – [Attributed to George Bernard Shaw] Concise Oxford Dictionary

The only thing in common between a bank treasury and a corporate treasury is the word “treasury”. Provide at least 10 arguments to support this statement.

[Exam question, Master of Applied Finance elective, Corporate Treasury Management, Macquarie University]

Different perspectives result in different patterns of behaviour. Understanding this can lead to significant opportunities to increase value and cash flow.

When I moved from running the currency operations of a major company into the Treasury of a large bank, it was like walking into to a parallel universe – yet even today the vast majority of bankers and corporate finance executives seem blissfully unaware of the fact, or its highly significant consequences.

The only thing in common between a bank treasury and a corporate treasury is the word “treasury”. Provide at least 10 arguments to support this statement.

[Exam question, Master of Applied Finance elective, Corporate Treasury Management, Macquarie University]

Different perspectives result in different patterns of behaviour. Understanding this can lead to significant opportunities to increase value and cash flow.

When I moved from running the currency operations of a major company into the Treasury of a large bank, it was like walking into to a parallel universe – yet even today the vast majority of bankers and corporate finance executives seem blissfully unaware of the fact, or its highly significant consequences.

The key differences

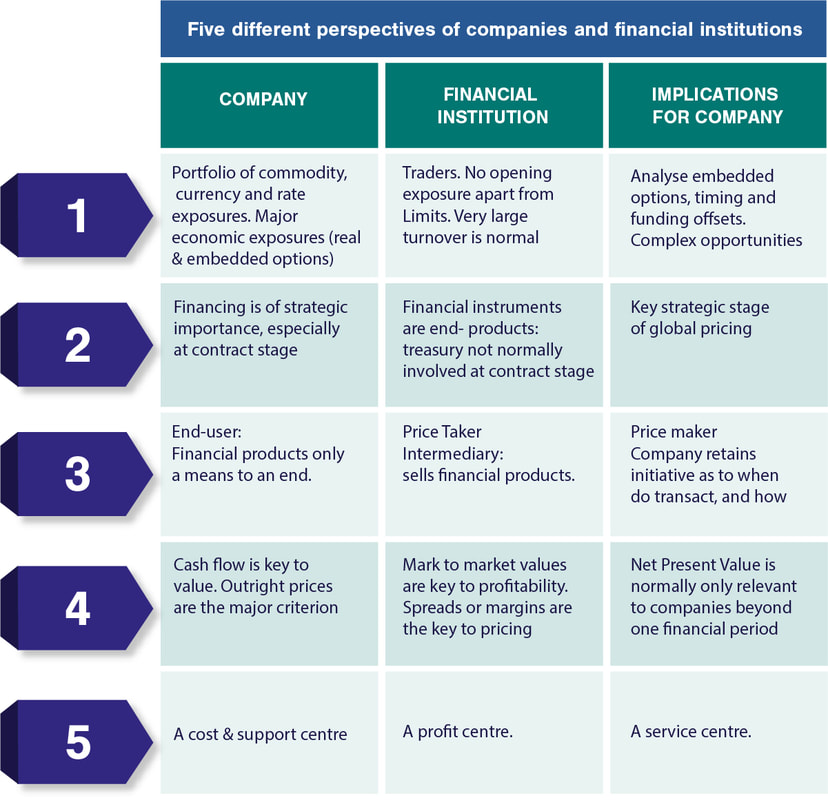

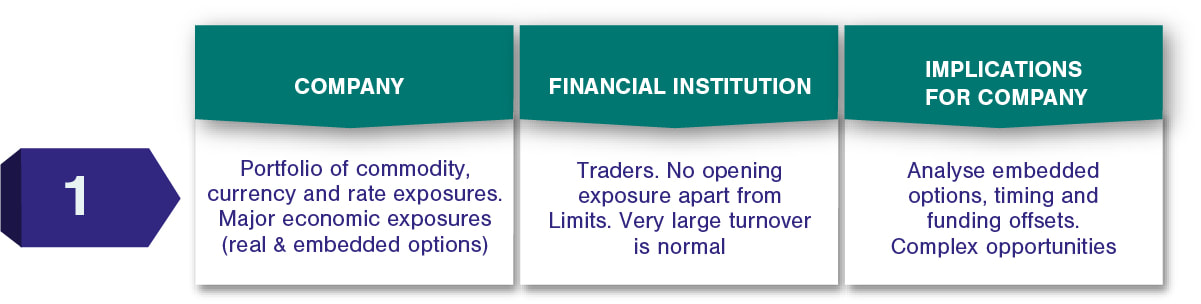

1. Companies start with an exposure cocktail – commodity, currency, capital & cash

Companies start with a commodity exposure, such as coal in the case of a miner or computers in the case of a computer company. Their foreign exchange exposure is either direct, as in both these cases, or indirect, where a company may become more competitive or less competitive simply because an exchange rate movement has changed their price effectiveness in global markets. For example, when the Australian Dollar appreciates, many domestic manufacturers lose market share as imports gain a price advantage purely due to this movement in exchange rates, rather than any change in relative productivity.

In addition, companies can have quite different time horizons, from a few months in the case of importers who can vary their source of supply to commodity exporters whose exposure extend out years.

Finally, there are often conditions within contracts that modify apparent exposures.

Identifying and valuing commercially-sourced options [embedded options]

Less than 10% of Australian-based companies purchase options and other derivatives from financial institutions.

However, the proportion of Australian companies with “live” option positions rises to above 80% when contract or commercially-based options are added. These embedded options are in the form of pricing clauses, re-pricing clauses, warranties, ceiling/floor pricing agreements, currency-related price-adjustment clauses and so on.

As these have exactly the same effect on the commercial outcome of a company’s activities as options and derivatives purchased from financial institutions, they need to be identified and quantified. Often, they are cheaper than those available from financial institutions, so arbitrage opportunities are common.

Financial institutions have an entirely different opening position. By central bank regulation they hold very limited open positions and what exposures they have are “pure” in the sense that they are not tied to commodity prices like sugar or wheat.

Implications for companies

Knowing your initial exposure to movements in currency rates is fundamental to a healthy business – and it can be complex. Contracts need to be analysed and both dangers and opportunities examined. Capital markets can often be part of the solution, because the two markets are closely linked.

In addition, companies can have quite different time horizons, from a few months in the case of importers who can vary their source of supply to commodity exporters whose exposure extend out years.

Finally, there are often conditions within contracts that modify apparent exposures.

Identifying and valuing commercially-sourced options [embedded options]

Less than 10% of Australian-based companies purchase options and other derivatives from financial institutions.

However, the proportion of Australian companies with “live” option positions rises to above 80% when contract or commercially-based options are added. These embedded options are in the form of pricing clauses, re-pricing clauses, warranties, ceiling/floor pricing agreements, currency-related price-adjustment clauses and so on.

As these have exactly the same effect on the commercial outcome of a company’s activities as options and derivatives purchased from financial institutions, they need to be identified and quantified. Often, they are cheaper than those available from financial institutions, so arbitrage opportunities are common.

Financial institutions have an entirely different opening position. By central bank regulation they hold very limited open positions and what exposures they have are “pure” in the sense that they are not tied to commodity prices like sugar or wheat.

Implications for companies

Knowing your initial exposure to movements in currency rates is fundamental to a healthy business – and it can be complex. Contracts need to be analysed and both dangers and opportunities examined. Capital markets can often be part of the solution, because the two markets are closely linked.

2. Major economic exposures

With global markets, competitive positions are continually adjusting but currency and commodity markets tend to adjust at quite different rates. This provides many short and long term windows of opportunity for companies as well as dangers. Companies need to see global opportunities in terms of local currencies – to have transparent global markets. Thus line managers and marketing executives can benefit greatly from understanding the consequences in terms of their own benchmarks – such as margins or Net Profit.

Financial Institutions have no such direct exposures.

There is a simple economic relationship:

Price X Quantity = Total Revenue [or Costs]

This is the equation faced by financial institutions. Cash flows are known because the products, such as forwards and swaps, involve contracted cash flows.

However, for any company and its competitors, this equation is more complicated. For companies, there are two prices, not one:

Price[commodity] X Price [currency] X Quantity = Total Revenue [or Costs].

These two prices are often interdependent and give companies a far more complex position to manage. The key stage for management is pre-contract

Financial Institutions have no such direct exposures.

There is a simple economic relationship:

Price X Quantity = Total Revenue [or Costs]

This is the equation faced by financial institutions. Cash flows are known because the products, such as forwards and swaps, involve contracted cash flows.

However, for any company and its competitors, this equation is more complicated. For companies, there are two prices, not one:

Price[commodity] X Price [currency] X Quantity = Total Revenue [or Costs].

These two prices are often interdependent and give companies a far more complex position to manage. The key stage for management is pre-contract

Often, contract pricing clauses can include embedded options such as currency adjustment clauses that allow one of the parties to re-invoice the other party should there be significant movements in exchange rate between the time the contract terms were agreed and settlement.

In fact we can we can make the following assertion:

For one party it is always better to use embedded options rather than adjust exposures through financial market dealings.

Foreign exchange is only a means to an endCompanies are price-takers when it comes to foreign exchange; financial institutions are price-makers.

Companies retain the initiative as to when to transact, as well as how to transact and with whom. Financial institutions must always be willing to quote a rate; companies have the right to accept or reject that quote.

Implications for companies

For companies, not using financial markets is often the preferred strategy, either by adjusting contract terms or by netting-off exposures or by pricing in local currencies. Further, they retain the ability to determine the timing of these decisions. For a company these are strategic decisions. For a financial institution, they are merely another trade.

In fact we can we can make the following assertion:

For one party it is always better to use embedded options rather than adjust exposures through financial market dealings.

Foreign exchange is only a means to an endCompanies are price-takers when it comes to foreign exchange; financial institutions are price-makers.

Companies retain the initiative as to when to transact, as well as how to transact and with whom. Financial institutions must always be willing to quote a rate; companies have the right to accept or reject that quote.

Implications for companies

For companies, not using financial markets is often the preferred strategy, either by adjusting contract terms or by netting-off exposures or by pricing in local currencies. Further, they retain the ability to determine the timing of these decisions. For a company these are strategic decisions. For a financial institution, they are merely another trade.

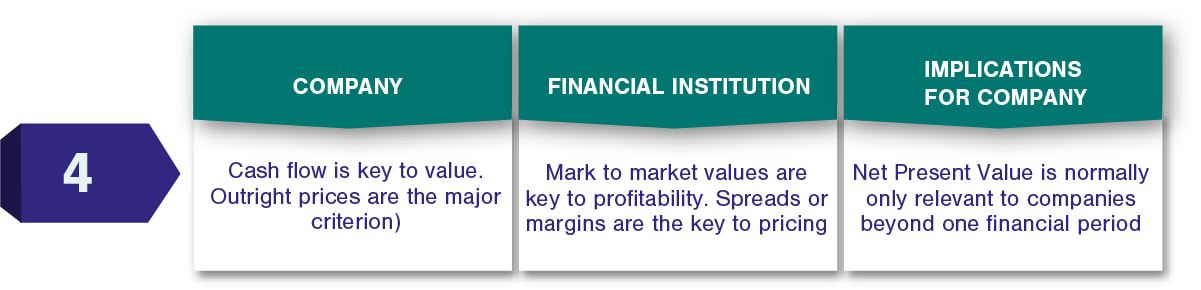

3. Company cash flow vs. financial institutions’ Mark to Market.

For most companies it is their cash flows that dominate their planning, strategic management and reporting, including calculations of Net Profit and financial incentives schemes such as bonuses. Thus, for example, future contracted sales of products are simply added up regardless of when the sales will take place. This is known as a “future value” approach to operations.

Financial institutions, on the other hand, adopt a policy of re-pricing all outstanding financial instruments such as foreign exchange forwards and options. This technique is known as “marking to market” and the result is the valuation of each product in terms of today’s prices, or their Net Present Values [NPVs].

This a classic case of parallel universes, as where the two intersect there is often great confusion.

This is particularly the case where the two methods are mixed and a combination of future values and present values emerges.

Some accounting policies allow some company exposures to be valued at future prices and others at present values.

This emphasis or profit and loss effects, rather than on the cash flow effects, can have major implications for both the treasurer and the company. As a US specialist puts it:

"Difficulties in distinguishing between the accounting description of foreign exchange risk and the business reality of the effects of these risks can cause corporate executives to make serious errors of judgment. In few other areas (outside the treatment of depreciation) is such a large divergence possible between a company’s actual and reported results.”

[Shapiro, A.C. Multinational Financial Management, Boston, Allyn and Bacon]

Financial institutions, on the other hand, adopt a policy of re-pricing all outstanding financial instruments such as foreign exchange forwards and options. This technique is known as “marking to market” and the result is the valuation of each product in terms of today’s prices, or their Net Present Values [NPVs].

This a classic case of parallel universes, as where the two intersect there is often great confusion.

This is particularly the case where the two methods are mixed and a combination of future values and present values emerges.

Some accounting policies allow some company exposures to be valued at future prices and others at present values.

This emphasis or profit and loss effects, rather than on the cash flow effects, can have major implications for both the treasurer and the company. As a US specialist puts it:

"Difficulties in distinguishing between the accounting description of foreign exchange risk and the business reality of the effects of these risks can cause corporate executives to make serious errors of judgment. In few other areas (outside the treatment of depreciation) is such a large divergence possible between a company’s actual and reported results.”

[Shapiro, A.C. Multinational Financial Management, Boston, Allyn and Bacon]

4. Corporate Profit Centre Treasuries are not beneficial

Less than 10% of companies have a formal treasury. The management of financial transactions is handled by a finance manager, controller or some similar person. In itself, this is no bad thing.

For companies, treasuries are optional; for financial institutions, essential.

The key issue to remember for company executives is that foreign exchange is a crucial part of the business’ strategic analysis and operations. The actual buying and selling of currencies or derivatives such as forwards is, in comparison, of trivial importance and can normally be delegated to a relatively junior position of responsibility or as a part of another more responsible role within the organisation.

For companies, treasuries are optional; for financial institutions, essential.

The key issue to remember for company executives is that foreign exchange is a crucial part of the business’ strategic analysis and operations. The actual buying and selling of currencies or derivatives such as forwards is, in comparison, of trivial importance and can normally be delegated to a relatively junior position of responsibility or as a part of another more responsible role within the organisation.

Consequences

The differences between the two approaches listed above mean that it is not far from the truth to say that the only thing that a company treasury has in common with a financial institution’s treasury is the word “treasury”. It is also true to say that most firms do not have a treasury, nor do they need one. However, all companies can benefit from access to global markets and therefore need some method of removing the fog of foreign exchange and being able to see different global strategies in terms of their own benchmarks.

The following section therefore examines the three main phases in exposure management and attempts to assist companies to answer the question:

”Are we comfortable with operating in a global market, or are we leaving most of the money lying on the table?”

The following section therefore examines the three main phases in exposure management and attempts to assist companies to answer the question:

”Are we comfortable with operating in a global market, or are we leaving most of the money lying on the table?”

Structuring corporate currency management

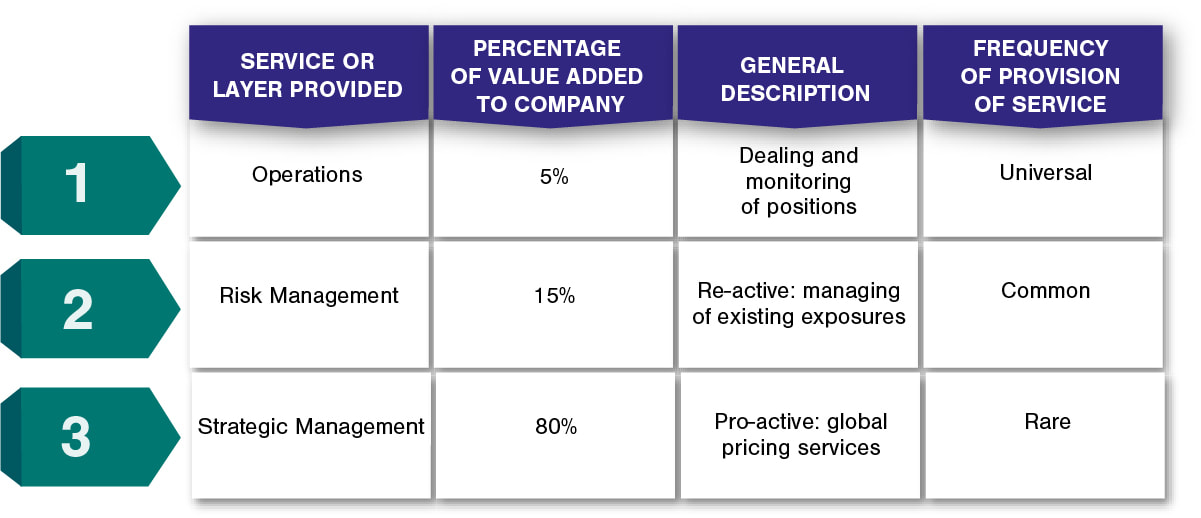

The three layers of foreign exchange services

Provision of strategic services

This layer of service has by far the greatest potential to add value.

It includes pro-active services such as pre-contract comparisons of pricing alternatives and assistance in contract negotiations, as well as the identification of windows of opportunity in global markets.

It involves bringing deals done in foreign currencies back to local currency terms so that there is no currency risk involved when comparing alternative pricing options.

One reason for the relative rareness of this function is that it does require access to the company’s marketing strategies and to information about contracts and projects prior to final agreement of the terms involved.

This service can be provided in-house in the case of larger companies or SMEs with potentially large exposures,

However, it can be outsourced since counterparty names and key contract details are not required to be passed on to a third party and various key levels of returns can be pre-set, triggering automatic notification should currency movements open market opportunities.

Given its potential to add value to a company, this is an area which should be considered by senior management as of crucial importance, as knowledge of strategic pricing alternatives can add substantially to profits and ignorance of it can mean unnecessarily giving excess margins to counterparties or to financial intermediaries involved in negotiations.

Frequency of the provision of this service: Uncommon, but understandably so. Few companies want or would even contemplate bringing in a financial institution to assist at this stage, for two main reasons:

This layer of service has by far the greatest potential to add value.

It includes pro-active services such as pre-contract comparisons of pricing alternatives and assistance in contract negotiations, as well as the identification of windows of opportunity in global markets.

It involves bringing deals done in foreign currencies back to local currency terms so that there is no currency risk involved when comparing alternative pricing options.

One reason for the relative rareness of this function is that it does require access to the company’s marketing strategies and to information about contracts and projects prior to final agreement of the terms involved.

This service can be provided in-house in the case of larger companies or SMEs with potentially large exposures,

However, it can be outsourced since counterparty names and key contract details are not required to be passed on to a third party and various key levels of returns can be pre-set, triggering automatic notification should currency movements open market opportunities.

Given its potential to add value to a company, this is an area which should be considered by senior management as of crucial importance, as knowledge of strategic pricing alternatives can add substantially to profits and ignorance of it can mean unnecessarily giving excess margins to counterparties or to financial intermediaries involved in negotiations.

Frequency of the provision of this service: Uncommon, but understandably so. Few companies want or would even contemplate bringing in a financial institution to assist at this stage, for two main reasons:

- the financial institution would be given commercially-sensitive information

- financial institutions make money from selling financial products, while many cases the purchase of a financial product would result in a sub-optimal solution.

Conclusion: A Board Perspective

Foreign Exchange as a strategic issue

Foreign exchange is seen in most companies in isolation, as a risk to be managed in much the same way as Operational Health & Safety.

With the demise of corporate treasuries as profit centres and the desire from company boards for “no surprises”, foreign exchange is normally seen as a necessary evil rather than a catalyst for generating long-term profits and company stability.

The operational aspects of foreign exchange management can be delegated to relatively junior executives within a company, or outsourced. It is the strategic aspects of foreign exchange in that are the key to enhanced long-term profitability. The aim is for company boards and senior management to be able to view global markets through a common and transparent common currency. This requires introducing this transparency at the planning stage - at the start of the currency pipeline.

Project profitability can thereby be enhanced, currency downside risks controlled or eliminated and market opportunities expanded.

A reluctance to act

For most senior executives, negotiating with financial institutions is like walking in to a pharmacy. There are on sale baffling arrays of products, some of which are different only in terms of their packaging. It is often preferable not to buy anything at all.

What is required is a preliminary visit to a doctor, an independent diagnosis of the symptoms and a prescription for the right solution.

Thus a company can construct its own self-diagnosis or call in a specialist to design one for them that can either be self-administered or monitored by the specialist.

The difficulty is to find a diagnostician that can be trusted, as the cure may otherwise be worse than the disease.

Such hesitance is natural, but clearly not an ideal state of affairs. What is required is a method that permits companies to obtain a proper diagnosis to ensure potential risks to corporate health are identified and controlled and opportunities to enhance the company’s robustness introduced.

A blueprint for strategic management to act

The simplest system for integrating global management into local strategies is to develop a system in the planning process that allows for pricing in either local or foreign currency but translating these into a common currency.

This responsibility would normally be handled by a company’s treasury, should one exist. In the majority of cases, it will be handled within the finance function, either directly or by obtaining independent pricing analysis.

The aim is to have a structure in place that captures the issue of global market access at the planning stage.

The key to this is benchmarking.

Foreign exchange is seen in most companies in isolation, as a risk to be managed in much the same way as Operational Health & Safety.

With the demise of corporate treasuries as profit centres and the desire from company boards for “no surprises”, foreign exchange is normally seen as a necessary evil rather than a catalyst for generating long-term profits and company stability.

The operational aspects of foreign exchange management can be delegated to relatively junior executives within a company, or outsourced. It is the strategic aspects of foreign exchange in that are the key to enhanced long-term profitability. The aim is for company boards and senior management to be able to view global markets through a common and transparent common currency. This requires introducing this transparency at the planning stage - at the start of the currency pipeline.

Project profitability can thereby be enhanced, currency downside risks controlled or eliminated and market opportunities expanded.

A reluctance to act

For most senior executives, negotiating with financial institutions is like walking in to a pharmacy. There are on sale baffling arrays of products, some of which are different only in terms of their packaging. It is often preferable not to buy anything at all.

What is required is a preliminary visit to a doctor, an independent diagnosis of the symptoms and a prescription for the right solution.

Thus a company can construct its own self-diagnosis or call in a specialist to design one for them that can either be self-administered or monitored by the specialist.

The difficulty is to find a diagnostician that can be trusted, as the cure may otherwise be worse than the disease.

Such hesitance is natural, but clearly not an ideal state of affairs. What is required is a method that permits companies to obtain a proper diagnosis to ensure potential risks to corporate health are identified and controlled and opportunities to enhance the company’s robustness introduced.

A blueprint for strategic management to act

The simplest system for integrating global management into local strategies is to develop a system in the planning process that allows for pricing in either local or foreign currency but translating these into a common currency.

This responsibility would normally be handled by a company’s treasury, should one exist. In the majority of cases, it will be handled within the finance function, either directly or by obtaining independent pricing analysis.

The aim is to have a structure in place that captures the issue of global market access at the planning stage.

The key to this is benchmarking.

RSS Feed

RSS Feed