Above all, what a Board wants from its finance function is: No Surprises.

Subject to that proviso, finance is seen as a key tool in assisting the Board and the rest of the organisation to achieving their company’s goals. Finance interacts at all levels in order to add value.

To that end, the Board and senior executives (collectively, the “C” Suite – CEO, CFO, COO, etc) want finance to provide crystal-clear advisory and operational services.

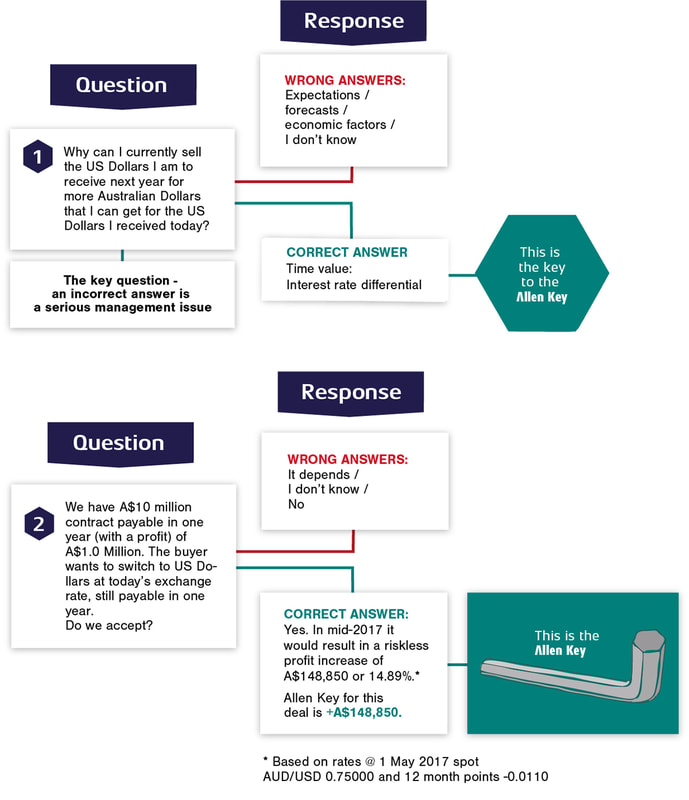

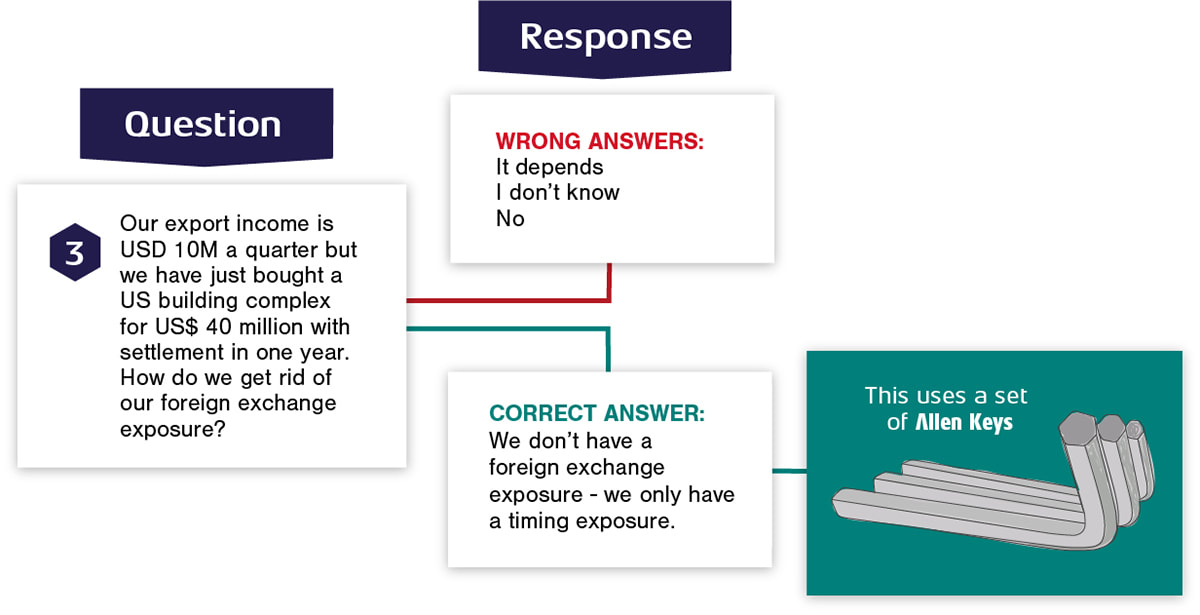

There is a tool which can be used by any member of the organisation to unlock financial value in commercial terms. The tool is primarily used by export and procurement functions, but it can also be used in constructing financial structures or taking them apart.

The tool is the Allen (or Hex) Key. It can be used for a single purpose or a part of a set (a key ring).

Subject to that proviso, finance is seen as a key tool in assisting the Board and the rest of the organisation to achieving their company’s goals. Finance interacts at all levels in order to add value.

To that end, the Board and senior executives (collectively, the “C” Suite – CEO, CFO, COO, etc) want finance to provide crystal-clear advisory and operational services.

There is a tool which can be used by any member of the organisation to unlock financial value in commercial terms. The tool is primarily used by export and procurement functions, but it can also be used in constructing financial structures or taking them apart.

The tool is the Allen (or Hex) Key. It can be used for a single purpose or a part of a set (a key ring).

It can be utilised by multinationals, SMEs, Not-for-profits and government entities.

Interactive Finance operates as a financial Global Positioning System (GPS).

The Board and senior executives drive the process, determining both the starting point and the goal or destination for the company as a whole and also for individuals with responsibilities to drive or direct operations.

Interactive Finance (in its role as a GPS) then provides the simplest direct financial route to get there – including timings, pricings and hazard identification.

Interactive Finance then provides optional alternative routes. These include contractual solutions, because every financial instrument can be replicated in a contract or commercial agreement. Alternate routes might involve capital market solutions or commercial market solutions – including economic or ‘real’ options.

Once the journey commences, proactive and reactive management systems kick in, reinforcing opportunities (as they appear through the windows) and reactive management triggers (on the ‘dashboard’) designed to minimise dangers, both anticipated and unexpected.

The Board and senior executives drive the process, determining both the starting point and the goal or destination for the company as a whole and also for individuals with responsibilities to drive or direct operations.

Interactive Finance (in its role as a GPS) then provides the simplest direct financial route to get there – including timings, pricings and hazard identification.

Interactive Finance then provides optional alternative routes. These include contractual solutions, because every financial instrument can be replicated in a contract or commercial agreement. Alternate routes might involve capital market solutions or commercial market solutions – including economic or ‘real’ options.

Once the journey commences, proactive and reactive management systems kick in, reinforcing opportunities (as they appear through the windows) and reactive management triggers (on the ‘dashboard’) designed to minimise dangers, both anticipated and unexpected.

Stage 1:

Goal setting: Role of the Board of Directors

Prior to the start of active Financial Management, the Board of Directors needs to resolve the enterprise’s operational ‘footprint’ in three areas:

Core targets or objectives: The goals of the enterprise – as diverse as mining & extraction, medical or mission work, government services or share market investments

Operational parameters: Stakeholder expectations, which will include issues of values and ethics.

Risk Tolerances: The Board sets the acceptable levels of risk, which drives the determination of benchmarks.

Core targets or objectives: The goals of the enterprise – as diverse as mining & extraction, medical or mission work, government services or share market investments

Operational parameters: Stakeholder expectations, which will include issues of values and ethics.

Risk Tolerances: The Board sets the acceptable levels of risk, which drives the determination of benchmarks.

Stage 2:

The value triumvirate: Profit Opportunity Price

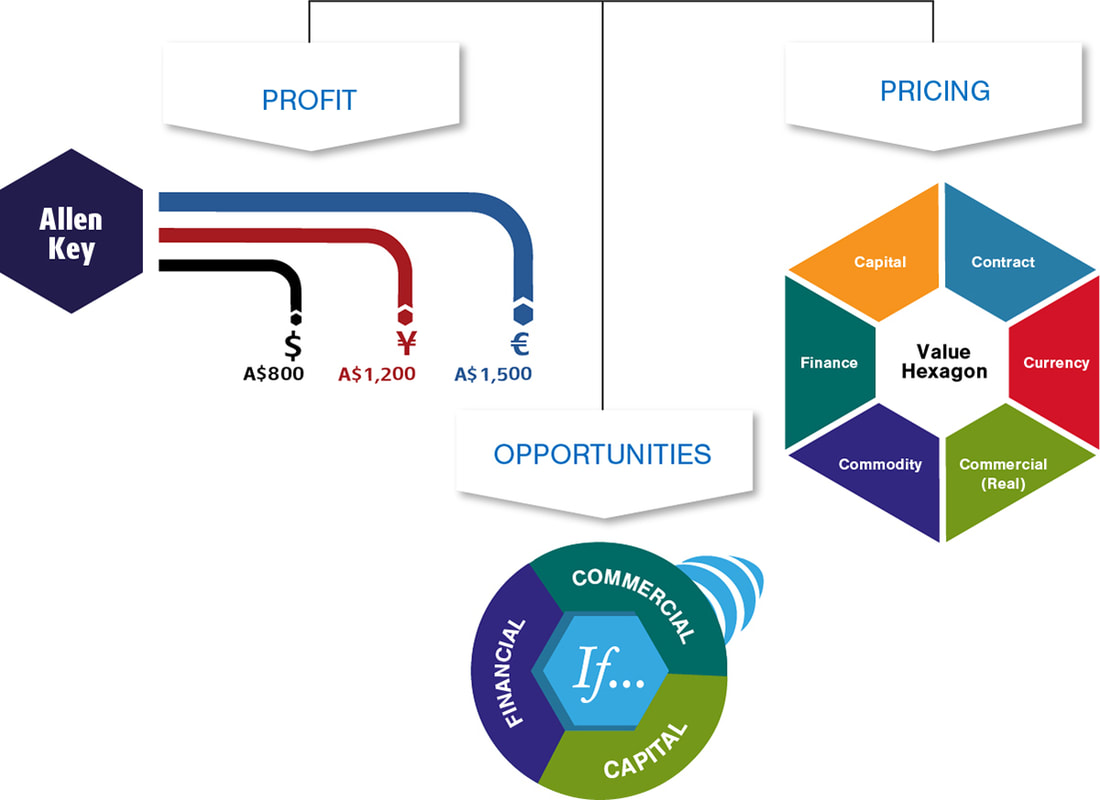

Profit, Opportunity and Price – triples your ability to add value.

A. Profit – transparent global prices & timings. Allen Key™ A$ price as benchmark regardless of currency of invoice.

B. Opportunities – If… Interactive Finance options (all opportunities are in fact real or economic options)

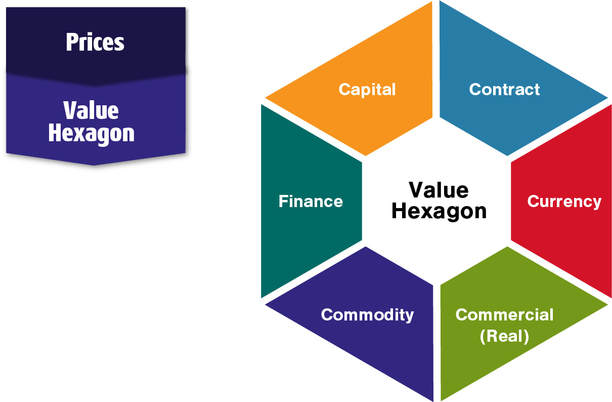

C. Price – Hex Key or Price Hexagon: Six times the horsepower of financial markets alone: Five Corporate (Capital, Commercial - real or economic - Commodity, Contract and Currency) plus Financial (instruments, derivatives & hybrids) - six sided pricing.

A. Profit – transparent global prices & timings. Allen Key™ A$ price as benchmark regardless of currency of invoice.

B. Opportunities – If… Interactive Finance options (all opportunities are in fact real or economic options)

C. Price – Hex Key or Price Hexagon: Six times the horsepower of financial markets alone: Five Corporate (Capital, Commercial - real or economic - Commodity, Contract and Currency) plus Financial (instruments, derivatives & hybrids) - six sided pricing.

A. Profit

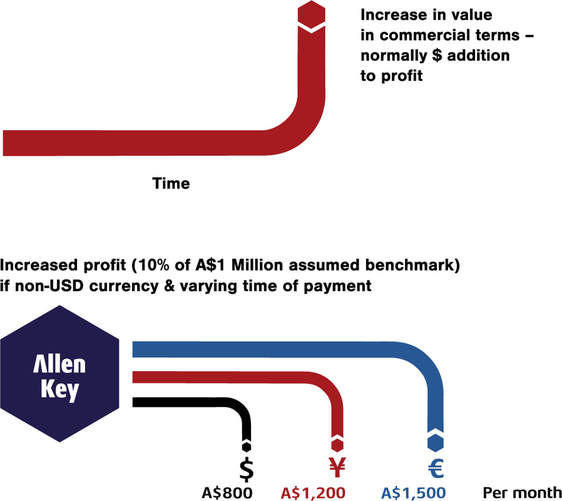

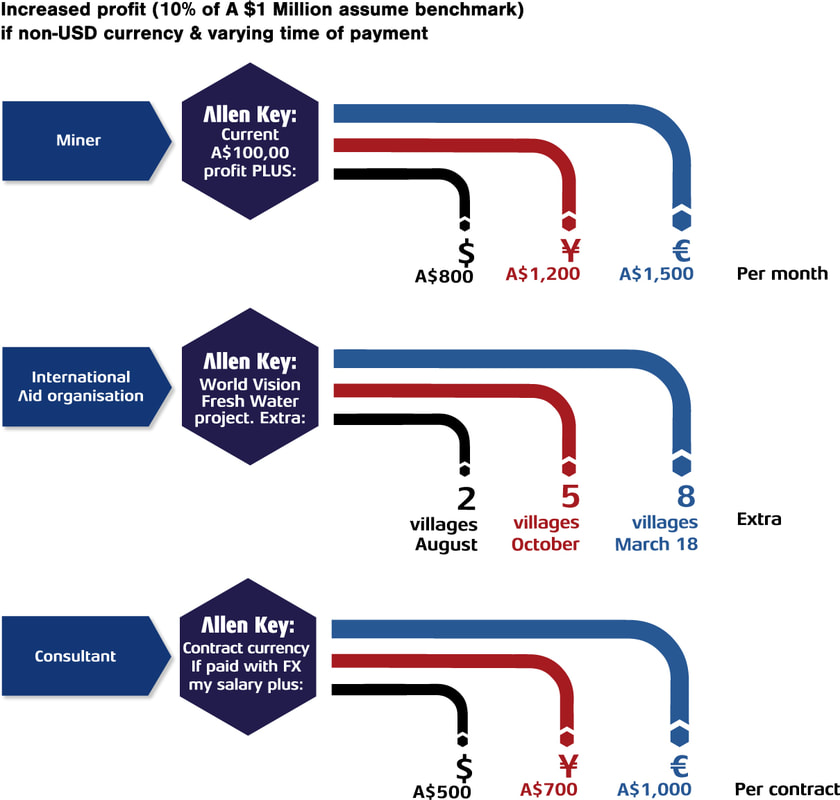

Profit – transparent global prices & timingsSelling your foreign exchange exposure adds to revenue and profit

Per A$ 1million of sales directly to profit and cash flow, add:

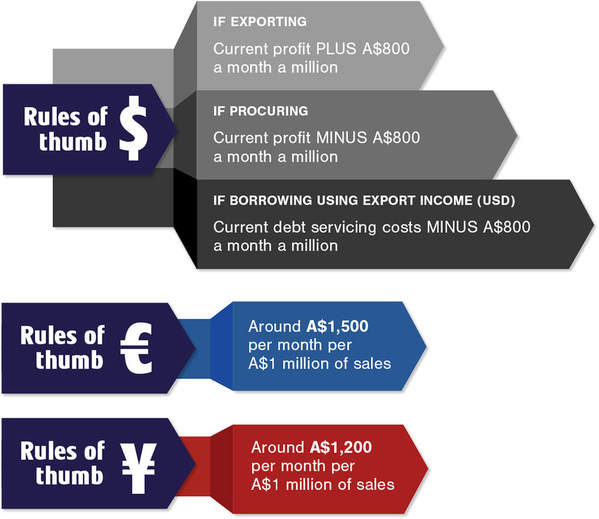

US Dollars: Around A$800 per month per A$ 1million of sales

Yen: Around A$1,200 per month per A$ 1million of sales

Euros: Around A$1,500 per month per A$ 1million of sales

100% of increased revenue goes directly to profits

Per A$ 1million of sales directly to profit and cash flow, add:

US Dollars: Around A$800 per month per A$ 1million of sales

Yen: Around A$1,200 per month per A$ 1million of sales

Euros: Around A$1,500 per month per A$ 1million of sales

100% of increased revenue goes directly to profits

This is additional, risk-free cash - no currency forecasting

These amounts are based on the forward or outright exchange rates available from virtually all banks.

obtaining the benefit of forward sales is to get at least two banks to quote a firm price.

And borrowing:

These amounts are based on the forward or outright exchange rates available from virtually all banks.

obtaining the benefit of forward sales is to get at least two banks to quote a firm price.

- Currency is managed as a commodity

- Forecasting is replaced with profit & risk triggers; scenario management, not speculation

And borrowing:

Every exporter should have a key cut to unlock the organisation’s key targets.

For example,

For example,

- Miner

- International aid organisation

- Consultant

B. Opportunities

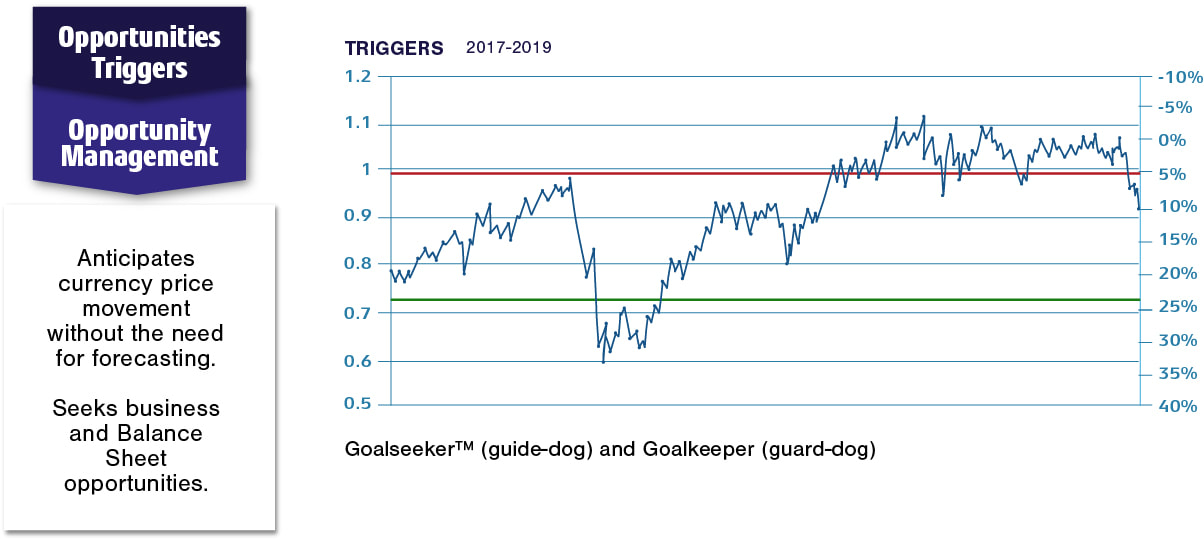

The diagram below identifies trigger levels (strike prices), but option opportunities for corporates are far wider - encompassing economic, real, financial, embedded, commercial, currency, commodity and capital.

Options are disruptive - they are challenging the status quo by focusing on value optimisation on the initiative of the company.

Options are disruptive - they are challenging the status quo by focusing on value optimisation on the initiative of the company.

C. Price: The Value Hexagon

Businesses can maximise global profits by adjusting returns

The Value Hexagon increases value or confirms value: it cannot reduce value.

The six price regimes now give companies the equivalent of a six-ring circus, rather than the single sourced dog-and-pony show.

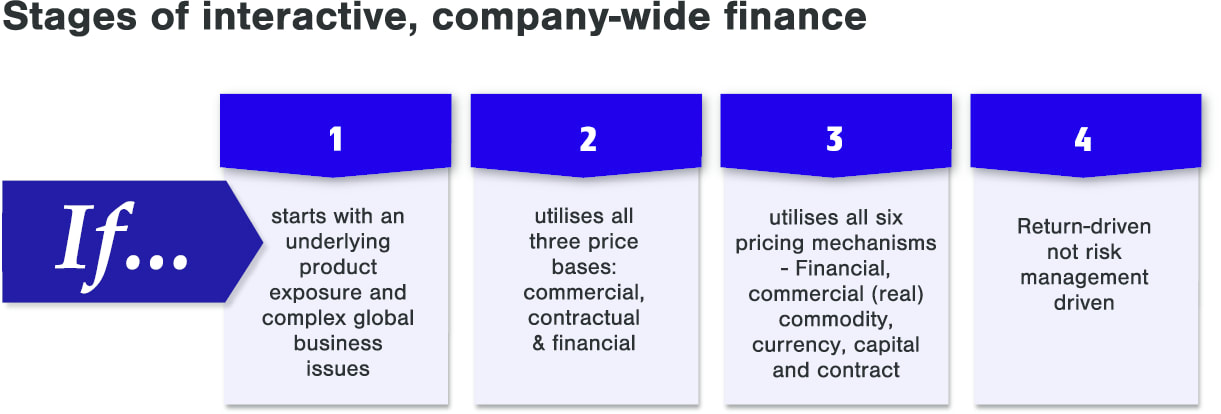

If… starts with an underlying product exposure and complex global business issues

- any time

- any risk/return trade-off

- any currency

The Value Hexagon increases value or confirms value: it cannot reduce value.

The six price regimes now give companies the equivalent of a six-ring circus, rather than the single sourced dog-and-pony show.

If… starts with an underlying product exposure and complex global business issues

- utilises all three price bases: commercial, contractual & financial and

- utilises all six pricing mechanisms – Financial, commercial (real) commodity, currency, capital and contract

- Return-driven not risk management driven

Stage 3:

The Six Sectors of Price Value Management

1. Contract. Currently, any contract for Australian exporters using US Dollars, Euros, Yen, Sterling etc to price at the current exchange rate (spot) benefits from the Allen Key approach – sell into Australian Dollars and add cash and profit.

However, even greater is the benefit from price adjustment clauses. Look for the word “IF” – it normally identifies an embedded option. If not there, try adding them – normally much more valuable than their financial market option instruments.

2. Currency. Includes swaps, forwards and options - which can be used to engineer hybrids. Covers a spectrum of financial engineering possibilities, all based on building from the standard simple tools of swaps, forwards and options.

3. Commercial: - Real or Economic options. These are often of crucial importance to business as they cover the economic ability to enter or leave markets (e.g. Abandonment options or exporters’ trigger options as listed under Opportunities). Often unidentified or either not priced at all or mispriced, they underpin both proactive and reactive management.

4. Commodity. Includes futures and options, both commercial and financial, as well as real commodity options. Commodity loans and investment and equity products are also common.

5. Capital. Debt and equity, primary and secondary, onshore and offshore – including options.

6. Financial. Bills, bonds, monetary instruments, options, forwards and swaps form the building blocks for financial markets and products. Their initial pricing is against a common Net Present Value of zero, which assists greatly in monitoring their value.

The Value Hexagon as a price matrixAlternatively, these markets can be grouped into three broader categories, providing commercial, contractual (legal) and financial pathways to pricing.

However, even greater is the benefit from price adjustment clauses. Look for the word “IF” – it normally identifies an embedded option. If not there, try adding them – normally much more valuable than their financial market option instruments.

2. Currency. Includes swaps, forwards and options - which can be used to engineer hybrids. Covers a spectrum of financial engineering possibilities, all based on building from the standard simple tools of swaps, forwards and options.

3. Commercial: - Real or Economic options. These are often of crucial importance to business as they cover the economic ability to enter or leave markets (e.g. Abandonment options or exporters’ trigger options as listed under Opportunities). Often unidentified or either not priced at all or mispriced, they underpin both proactive and reactive management.

4. Commodity. Includes futures and options, both commercial and financial, as well as real commodity options. Commodity loans and investment and equity products are also common.

5. Capital. Debt and equity, primary and secondary, onshore and offshore – including options.

6. Financial. Bills, bonds, monetary instruments, options, forwards and swaps form the building blocks for financial markets and products. Their initial pricing is against a common Net Present Value of zero, which assists greatly in monitoring their value.

The Value Hexagon as a price matrixAlternatively, these markets can be grouped into three broader categories, providing commercial, contractual (legal) and financial pathways to pricing.

Hex Key: KEY PRICING & VALUATION PATHWAYS

There are normally three but always at least two ways of pricing or valuing a position or proposal and one will virtually always be superior (Law of Two Prices):

Business Advantages

If…

- Contractual Contract pricing clauses and repricing & value variation clauses. Virtually all financial contracts can be replicated through commercial contracts

- Financial Standard financial instruments plus derived or synthetic financial engineering

- Commercial Real (economic) options. Common often overlooked and potentially highly valuable

- Price verification Determines which of the three parallel sectors of financial, contractual and commercial provides the best value.

- Arbitrage Takes any available pricing advantage from ‘mismatches’ between the three parallel markets - financial, contractual and commercial.

- Control This stage is also called ‘stage-gating’. It ensures there is no price gouging or any hidden charges or fees.

Business Advantages

If…

- Turns Business Units from treasury clients into co-workers & vastly improves effectiveness

- Connects with business areas earlier & at both executive and operational levels

- Provides enterprises with global pricing support for marketing & sales, procurement, purchasing and funding and financial management.

- Replaces a reliance on external treasury & bank advisory personnel and greatly enhances financial strategic and operational support to Business and support centres.

- Coverage: Financial markets (funding & financing), Commodities and share markets; Currencies & cash flows; equities & investments

Key questions for the Board to ask prospective Finance Executives

Recommendations to the Board:

Global Price Management

Recommendations to the Board: Global Price Management

1. Set business-related goals Goals such as return on assets or net profit should be used, not currency forecasts.

2. Conduct a global finance audit (POP) This is only required about once a year. Look for both opportunities and risks. Audit all major contracts, including equipment purchases, for embedded options.

3. Determine sensitivities and key levels Pre-set trigger levels and sunset clauses. Determine critical financial and economic levels for opportunistic profits and dangers. Set automatic reviews set, e.g. for the structure of your finance function.

4. Set benchmarks Benchmarks bias behavior - and the absence of a clear benchmark may result in "Monitor carefully but do nothing" being adopted, giving form but not substance to the management process. This default means that many of the opportunities to increase profits are not properly evaluated.

5. Structure responsibilities, from Board to Treasury. It is important that the Board determines the structure of its financial function at the final stage rather than prior to developing the business strategy, because most of the key strategies will already be in place. All that may be left is managing the transactions, monitoring, dealing and recording/auditing. The final "treasury" options are:

1. Set business-related goals Goals such as return on assets or net profit should be used, not currency forecasts.

2. Conduct a global finance audit (POP) This is only required about once a year. Look for both opportunities and risks. Audit all major contracts, including equipment purchases, for embedded options.

3. Determine sensitivities and key levels Pre-set trigger levels and sunset clauses. Determine critical financial and economic levels for opportunistic profits and dangers. Set automatic reviews set, e.g. for the structure of your finance function.

4. Set benchmarks Benchmarks bias behavior - and the absence of a clear benchmark may result in "Monitor carefully but do nothing" being adopted, giving form but not substance to the management process. This default means that many of the opportunities to increase profits are not properly evaluated.

5. Structure responsibilities, from Board to Treasury. It is important that the Board determines the structure of its financial function at the final stage rather than prior to developing the business strategy, because most of the key strategies will already be in place. All that may be left is managing the transactions, monitoring, dealing and recording/auditing. The final "treasury" options are:

- T1: Cost Centre: Operations-based. Strong focus on cash and working capital management. In fact, the Americans call their equivalent of the British Corporate Treasurers Association the Cash Management Association.

- T2: Service Centre: T1 plus financial risk management

- T3: Strategy Centre: T2 plus enterprise-wide interactive financial management

- T4: Profit Centre: Leave this to the banks, who are professionals. It is set up as a Business Unit - creating disruptive internal competition. Rare these days - and it is recommended that it stays that way.

RSS Feed

RSS Feed