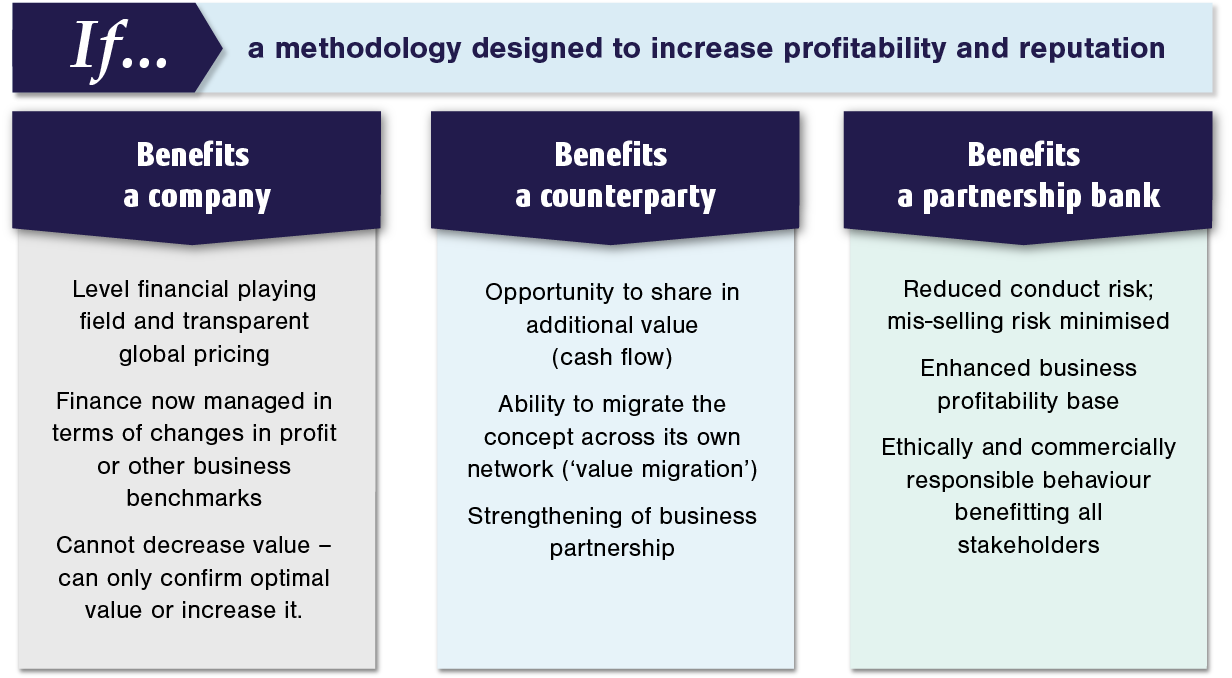

Interactive Finance claims to:

It involves identifying pricing arbitrages as well as windows of opportunity.

- Provide a win/win/win solution option for a company + its counterparty + its bank.

- make global pricing transparent

- Use price relativities to identify if value can be increased

It involves identifying pricing arbitrages as well as windows of opportunity.

Some answers:

1. People are already doing it – but they do not advertising the fact because they presumably want all the benefits rather than sharing them –“knowledge arbitrage”. There’s a saying in the foreign exchange market, “If you can’t see the wood duck, you’re it”. For ethical reasons, Interactive Finance does advertising the fact - and the resulting market transparency.

2. Institutional blockages– especially large corporations, governments and supranationals. An example also quoted in IF's CFO’s Financial Engineering Handbook is an ignored A$1.2 Billion arbitrage 17 years ago (and every 3 years since then):

The genesis of this case is the 2000 World Bank member subscription agreement for 2000 – 2002. Details were freely available on the web at http://www.worldbank.org/ida/ida12/index.htm, and this specific case was therefore used to teach Master of Applied Finance students as a ‘live’ example

The Japanese could have paid JPY 213,659.19 million - a saving of JPY 81,393.67 million - equal to AUD 1,217 million [AUD 1.2 billion] - without any net currency exposure, and which they could have donated to the World Bank as a further contribution. Yet they didn’t. In Australia’s case a more modest A$230 Million could have been saved. It wasn’t.

In 2017 little has changed. Australian and state governments are potentially looking at around the billion dollar mark in potential savings on projects including tollways and submarines. In addition, in some cases multinationals such as Chevron are claiming more money in tax deductions than the original capital cost of projects – see later in the Handbook for details about ‘snowballing’. [The CFO’s Financial Engineering Handbook]

Most contracts involving foreign exchange are priced beneficially to one party – but not challenged. Many contain “Allen Keys” – additional profits.

3. Corporates and financial institutions operate in Parallel Markets, using different value benchmarks: banks and corporates do not focus on the same measure of profitability, leaving “time value” to atrophy – to erode, rather than being captured. Banks concentrate on Present Value (mark-to Market) while corporates focus on Cash Flow or Future Value. The difference is time value – which is captured in the Allen Key.

For most companies it is their cash flows that dominate their planning, strategic management and reporting, including calculations of Net Profit and financial incentives schemes such as bonuses. Thus, for example, future contracted sales of products are simply added up regardless of when the sales will take place. This is known as a “future value” approach to operations.

Financial institutions, on the other hand, adopt a policy of re-pricing all outstanding financial instruments such as global pricing forwards and options. This technique is known as “marking to market” and the result is the valuation of each product in terms of today’s prices, or their Net Present Values [NPVs].

This classic case of parallel universes occurs because Banks don't see the value to corporates because they are not looking for it.

Time value dollars are left on the table.

[See the article on Parallel Universes on LinkedIn or at www.giffnock.com ]

4. Multinational interests divert value offshore or to shareholders: transfer pricing and tax minimisation techniques are used rather than If’s value optimisation. A 2017 judgement in favour of the Australian Tax Office and against the oil multinational Chevron illustrates this point well.

2. Institutional blockages– especially large corporations, governments and supranationals. An example also quoted in IF's CFO’s Financial Engineering Handbook is an ignored A$1.2 Billion arbitrage 17 years ago (and every 3 years since then):

The genesis of this case is the 2000 World Bank member subscription agreement for 2000 – 2002. Details were freely available on the web at http://www.worldbank.org/ida/ida12/index.htm, and this specific case was therefore used to teach Master of Applied Finance students as a ‘live’ example

The Japanese could have paid JPY 213,659.19 million - a saving of JPY 81,393.67 million - equal to AUD 1,217 million [AUD 1.2 billion] - without any net currency exposure, and which they could have donated to the World Bank as a further contribution. Yet they didn’t. In Australia’s case a more modest A$230 Million could have been saved. It wasn’t.

In 2017 little has changed. Australian and state governments are potentially looking at around the billion dollar mark in potential savings on projects including tollways and submarines. In addition, in some cases multinationals such as Chevron are claiming more money in tax deductions than the original capital cost of projects – see later in the Handbook for details about ‘snowballing’. [The CFO’s Financial Engineering Handbook]

Most contracts involving foreign exchange are priced beneficially to one party – but not challenged. Many contain “Allen Keys” – additional profits.

3. Corporates and financial institutions operate in Parallel Markets, using different value benchmarks: banks and corporates do not focus on the same measure of profitability, leaving “time value” to atrophy – to erode, rather than being captured. Banks concentrate on Present Value (mark-to Market) while corporates focus on Cash Flow or Future Value. The difference is time value – which is captured in the Allen Key.

For most companies it is their cash flows that dominate their planning, strategic management and reporting, including calculations of Net Profit and financial incentives schemes such as bonuses. Thus, for example, future contracted sales of products are simply added up regardless of when the sales will take place. This is known as a “future value” approach to operations.

Financial institutions, on the other hand, adopt a policy of re-pricing all outstanding financial instruments such as global pricing forwards and options. This technique is known as “marking to market” and the result is the valuation of each product in terms of today’s prices, or their Net Present Values [NPVs].

This classic case of parallel universes occurs because Banks don't see the value to corporates because they are not looking for it.

Time value dollars are left on the table.

[See the article on Parallel Universes on LinkedIn or at www.giffnock.com ]

4. Multinational interests divert value offshore or to shareholders: transfer pricing and tax minimisation techniques are used rather than If’s value optimisation. A 2017 judgement in favour of the Australian Tax Office and against the oil multinational Chevron illustrates this point well.

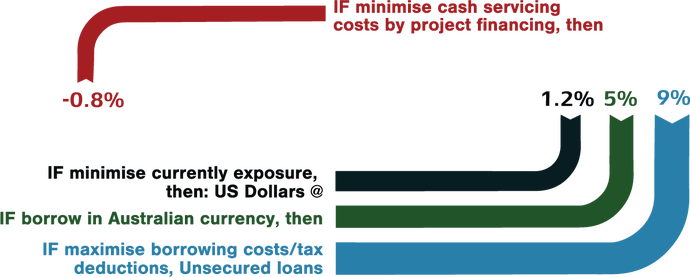

Chevron Tax Case

The Chevron case was based on a $US2.45 billion loan between the company's US and Australian operations.

The ATO claims a US-based entity raised the loan at an interest rate of 1.2 per cent. It then allegedly on-lent the money to the Australian entity at an interest rate of 9 per cent. The process is alleged to have netted Chevron up to $862 million in tax-free dividends over five years.

Interactive Finance’s Value Hexagon methodology identifies a further opportunity for Chevron’s Australian entity Caltex to pay -0.8% instead of 1.2% - or to simply borrow Australian Dollars in the wholesale market at 5%.

This leaves

- IF: an offshore parent can borrow at 1.2% and charge (AUD) 9%

- IF Arm’s length Australian subsidiary could borrow at (AUD) 5%

- IF Arm’s length Australian subsidiary could borrow at (USD) 1.2%

- IF Independent Australian exporter, could

- Borrow USD 1.2% but delay drawdown

- Sell forward into AUD benefitting from interest differential

- Repay in USD out of export revenue

At 8% the tax deduction equals the size of the underlying borrowing within 8 years – and effectively the overseas parent is able to reduce its overall tax payable to a fraction of nominal tax rates

5. Contracts are mis-specified, either by omission or by commission.

If the spot price is the basis of pricing but settlement is not immediate, then there is a floating value (time value) not identified UNLESS there is a repricing clause or similar embedded option.

Some massive mis-pricing and/or excess profits have resulted, especially in long term contracts, capital borrowings and project financings. A simple example may help illustrate this point.

If the spot price is the basis of pricing but settlement is not immediate, then there is a floating value (time value) not identified UNLESS there is a repricing clause or similar embedded option.

Some massive mis-pricing and/or excess profits have resulted, especially in long term contracts, capital borrowings and project financings. A simple example may help illustrate this point.

Recent example: Selling real estate (based on actual rates in 2016)

A contract to purchase a Sydney office building stated:

The price of the Real Estate you wish to buy is A$10 million but IF you prefer, the US Dollar equivalent at the current exchange rate. These words are valuable. They are the equivalent of a financial option. They can be used to enhance returns or on occasion even be sold to third parties.

In this case, the sale involved a $10 million Sydney property to an overseas purchaser

what IF... You had sold a property for A$ 10 million to a US buyer?

(This makes you a profit of A$1,000,000)

what IF... Settlement won’t be for a year?

what IF... the buyer would be delighted to switch to US Dollars? Current spot exchange: USD 7,300,000

what IF... that will mean that you (or the agent or the US buyer – that’s where the ethics issue lies) will receive/share in an additional cash difference of A$ 167,000 because the 1 year outright rate on USD 7.3M was A$10,167,644 - a 16.7% increase in profit.

[See the Exporter’s Handbook for full details].

The price of the Real Estate you wish to buy is A$10 million but IF you prefer, the US Dollar equivalent at the current exchange rate. These words are valuable. They are the equivalent of a financial option. They can be used to enhance returns or on occasion even be sold to third parties.

In this case, the sale involved a $10 million Sydney property to an overseas purchaser

what IF... You had sold a property for A$ 10 million to a US buyer?

(This makes you a profit of A$1,000,000)

what IF... Settlement won’t be for a year?

what IF... the buyer would be delighted to switch to US Dollars? Current spot exchange: USD 7,300,000

what IF... that will mean that you (or the agent or the US buyer – that’s where the ethics issue lies) will receive/share in an additional cash difference of A$ 167,000 because the 1 year outright rate on USD 7.3M was A$10,167,644 - a 16.7% increase in profit.

[See the Exporter’s Handbook for full details].

Interactive Finance (IF) is

– Transparent

– Ethical

– Profitable

IF... Ethical financial management for a global marketplace

Utilises a company’s goals and sensitivities to market and price volatility in partnership with a bank’s systems, global presence, pricing and products to meet bank and client targets, reinforcing upside benefits while controlling downside risk.

The company drives the process.

The company determines the starting point and destination.

Interactive Finance tools then provides the simplest direct financial route to get there – including timings, pricings and hazard identification. If the company knows where they start and where they want to finish, an initial solution is provided (literally in seconds). This is then subjected to profit, pricing and opportunity (POP) analysis.

Interactive Finance tools then provides the simplest direct financial route to get there – including timings, pricings and hazard identification. If the company knows where they start and where they want to finish, an initial solution is provided (literally in seconds). This is then subjected to profit, pricing and opportunity (POP) analysis.

- Value optimisation as the core objective.

- Accessible by all levels of management, from Board to treasury

- Driven by corporate goals using corporate language & benchmarks. The importance of this should not be under-estimated.

RSS Feed

RSS Feed